2023 Changes to R&D Tax Relief: Explained

From 1st April 2023, a number of changes to R&D Tax Relief will come into effect.

The changes which were announced in the Autumn Budget 2021 and Autumn Statement 2022, represent some of the most substantial updates to the scheme since its inception over 20 years ago and will affect many companies’ future R&D claims.

We highlight the changes below, the associated timeframes and the impact they may have on your upcoming claim.

Adjustment to rates of R&D tax relief

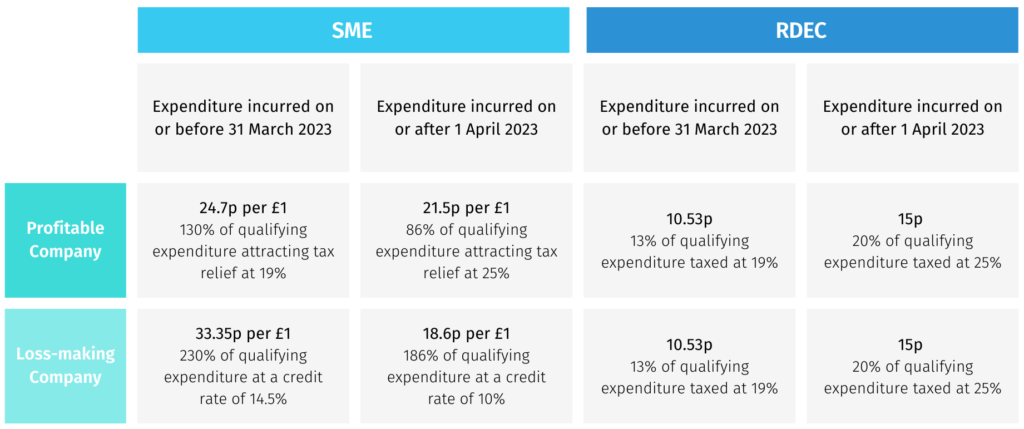

At Autumn Statement the Chancellor announced that as part of the ongoing R&D tax reliefs review, R&D tax relief rates would change from 1st April 2023:

- The RDEC rate will increase from 13% to 20%

- The SME additional deduction will decrease from 130% to 86%

- The SME credit rate will decrease from 14.5% to 10%

Changes to the rates coincide with changes to the corporation tax rate from 19% – 25%. The table below highlights the headline benefits for both the SME and RDEC schemes:

What does this mean for companies claiming under the RDEC scheme?

The RDEC rate increase from 13% to 20% equates to a circa 42% uplift in benefit received. The increase will improve the competitiveness of the scheme and hopefully result in a significant increase in investment in R&D, underpinning the government’s growth strategy. The change also moves a step towards a simplified, single RDEC-like scheme for all.

What does this mean for companies claiming under the SME scheme?

For innovative SME companies, the scheme becomes less attractive and may result in a reduction in their R&D investment. The greatest cost reduction will fall on start-up’s and loss-making companies that are most in need of the funding.

When do the R&D tax relief rate changes come in to effect?

The rate changes will affect R&D expenditure incurred on or after 1st April 2023. It is therefore important to note that companies who do not have a 31st March year end will need to apportion their qualifying R&D expenditure for periods that straddle 1st April 2023 to ensure that the correct rates are applied.

For example, a company with a 31st December year end will be able to claim for three months at the current rate and nine months at the new rate.

In addition to the SME & RDEC rate changes, there are a number of other changes that will take effect from 1st April 2023:

Overseas Expenditure

For both SME and RDEC schemes, overseas R&D costs recharged to a UK claimant company currently qualify for R&D tax relief. However, from 1st April 2023 R&D activity will have to be physically located in the UK to qualify. Therefore, costs associated with overseas subcontractors and externally provided workers (EPW’s) will in most cases, no longer be eligible for relief.

To class as qualifying expenditure under the new legislation, the expenditure on payments for subcontractors or EPW’s must be subject to PAYE and National Insurance Contributions (NICs), unless it counts as qualifying overseas expenditure. To count as qualifying overseas expenditure (QOE), the EPW’s or subcontractors must meet the following three criteria:

- The conditions necessary for the R&D are not present in the UK

- The conditions are present in the location where the R&D is undertaken

- It would be wholly unreasonable to replicate the conditions in the UK

An example of this scenario would be if the R&D involved placing sensors on active volcanoes. This requires a condition (the presence of a volcano) that is not present in the UK, and one which it would be wholly unreasonable to replicate. As it is a condition that exists in places outside the UK, this activity would be classed as QOE.

The changes to overseas expenditure will apply to accounting periods on or after 1st April 2023. The impact of this change will largely depend on the size of the claimant’s business and the amount of R&D taking place outside the UK. However, it will be a likely blow to smaller companies who cannot afford to pay fees of a UK provider.

Inclusion of Cloud Computing, Data and Mathematics Costs

For accounting periods starting on or after 1st April 2023, certain cloud computing, data licensing and mathematics costs will be eligible for relief when they directly contribute to the resolution of scientific or technological uncertainty.

Where data or cloud services are used for multiple purposes within the business (i.e., both inside and outside of R&D) you will be able to claim relief on a ‘reasonable apportionment’ of the associated costs.

Data that has been gathered internally, rather than licenced, will not qualify. However, staff costs associated with creating the dataset will be eligible.

The government is also updating the R&D tax relief guidelines to clarify that activities relating to pure mathematics now meet the definition and will be eligible for relief.

Cloud computing and licence payments for datasets are considerable costs for businesses, and these positive changes will allow them to claim relief on a wider range of expenditure from 1st April 2023.